Market Update | Second Quarter 2026

July 17, 2026

Key Highlights to Keep You Informed

The second quarter was shaped by geopolitical uncertainty, evolving expectations for interest rates, and continued investment in artificial intelligence (AI). While these developments created periods of market volatility, the underlying economy remained resilient and global markets finished the quarter higher.

Although headlines changed throughout the quarter, our investment approach did not. We remained focused on what we can control: thoughtful portfolio construction, attention to fundamentals, and helping clients stay the course through shifting market conditions.

Geopolitical Uncertainty Increased Market Volatility

Conflict in the Middle East disrupted shipping through the Strait of Hormuz, contributing to higher oil prices and unsettled markets. As diplomatic efforts progressed during June, oil prices moderated and market conditions improved. Although geopolitical risks remain, the quarter served as another reminder that markets often look beyond short-term uncertainty and refocus on long-term economic fundamentals.

U.S. Equities Delivered A Strong Recovery

Following weakness earlier in the year, U.S. stocks rebounded sharply during the second quarter.

- The S&P 500 gained approximately 15%.

- The Nasdaq Composite advanced roughly 21%, its strongest quarterly return since 2020.

Some of the largest cloud and technology companies, the so-called "hyperscalers" that have been heavily investing in data center development, saw their stock prices come under pressure amid concerns that heavy spending may outpace the eventual payoff. Technology companies, particularly semiconductor manufacturers benefiting from continued investment in AI infrastructure, drove much of the market's performance. The rebound underscores the difficulty of timing markets; investors who stayed invested through the spring weakness were rewarded.

The Federal Reserve Entered A New Chapter

Kevin Warsh assumed the role of Federal Reserve Chair during the quarter, replacing Jerome Powell after nearly eight years in the position. Many investors anticipated a more accommodative monetary policy under the new leadership. However, the Federal Open Market Committee elected to leave interest rates unchanged during its June meeting, emphasizing that inflation remains above the Federal Reserve's long-term objective. Future interest rate decisions will continue to be driven by incoming economic data rather than predetermined timelines. For investors, this reinforces the importance of maintaining diversified portfolios that can adapt across a range of economic and interest rate environments.

Artificial Intelligence Remains An Important Investment Theme

Investment in artificial intelligence infrastructure continued at a rapid pace during the quarter. Companies building semiconductors, data storage, networking equipment, and computing capacity benefited from increasing demand, even as investors began questioning whether elevated spending will translate into sustainable long-term earnings growth. That tension was on display in the quarter's most notable market event: SpaceX's long-awaited IPO. The $75 billion offering was the largest ever, surpassing Saudi Aramco's 2019 record of $29.4 billion, and its $1.77 trillion market value against $18.7 billion in 2025 revenue implies roughly 95 times annual revenue, far richer than virtually any other large public company (Nvidia trades near 20 times sales, Palantir at 57). With only about 5% of shares offered to the public, volatility has been elevated. IPOs from other major AI companies, including Anthropic and OpenAI, are anticipated in the coming months. Innovation remains one of the most powerful drivers of long-term economic growth. However, successful investing requires balancing excitement around transformational technologies with careful evaluation of valuations, competitive positioning, and sustainable earnings potential.

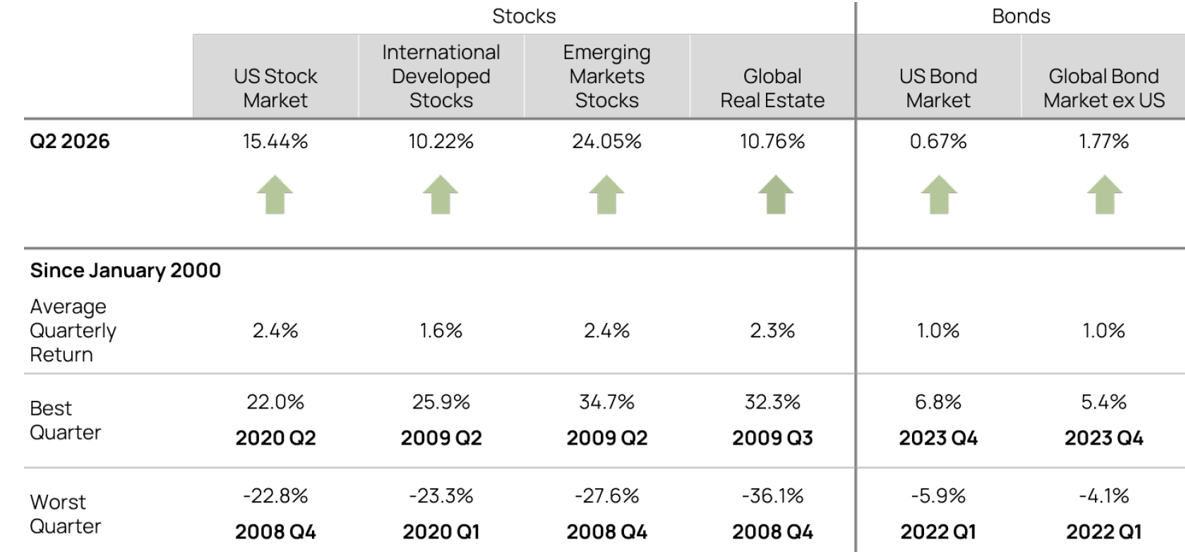

Quarterly Market Summary

Returns (USD), as of June 30, 2026

Past performance is not a guarantee of future results. Indices are not available for direct investment. Index performance does not reflect the expenses associated with the management of an actual portfolio.

Market segment (index representation) as follows: US Stock Market (Russell 3000 Index), International Developed Stocks (MSCI World ex USA Index [net dividends]), Emerging Markets (MSCI Emerging Markets Index [net dividends]), Global Real Estate (S&P Global REIT Index [net dividends]), US Bond Market (Bloomberg US Aggregate Bond Index), and Global Bond Market ex US (Bloomberg Global Aggregate ex-USD Bond Index [hedged to USD]). S&P data © 2026 S&P Dow Jones Indices LLC, a division of S&P Global. All rights reserved. Frank Russell Company is the source and owner of the trademarks, service marks, and copyrights related to the Russell Indexes. MSCI data © MSCI 2026, all rights reserved. Bloomberg data provided by Bloomberg.

Notable Events in Q2:

April

Global markets began the quarter facing heightened geopolitical uncertainty as conflict in the Middle East disrupted energy markets and global trade. Oil prices increased while the International Monetary Fund modestly lowered its outlook for global economic growth to 3.1% for 2026. Despite these headwinds, U.S. corporate earnings remained resilient and global stocks rebounded from a weak start to the year.

May

Markets continued to recover from the March downturn related to the conflict in the Middle East as the S&P 500 and Nasdaq both hit new highs, driven by strength in technology stocks. This came despite inflation reaching its highest rate in three years, as the PCE price index, the Fed's preferred inflation measure, rose 3.8% year over year, with oil prices holding near $100 a barrel. May also extended a streak of stronger-than-expected jobs reports as the U.S. economy added 172,000 nonfarm payroll jobs, ahead of the consensus estimate for 85,000, and unemployment held steady at 4.3%.

June

Diplomatic negotiations between the United States and Iran continued throughout June, culminating in a memorandum of understanding on June 17 aimed at ending the conflict. The agreement temporarily eased concerns over global energy supplies, contributing to a decline in Brent crude oil prices from approximately $98 per barrel at the beginning of the month to $71 by month end. While tensions persisted and subsequent events highlighted the fragility of the agreement, lower oil prices helped reduce inflation concerns and improve market sentiment.

Kevin Warsh chaired his first Federal Open Market Committee meeting after succeeding Jerome Powell as Federal Reserve Chair. The Committee left interest rates unchanged at 3.5% to 3.75%, while reaffirming its commitment to returning inflation to its 2% target.

The FIFA World Cup also began during the quarter, with matches hosted across the United States, Canada, and Mexico. While historical evidence suggests the long-term economic benefits for host cities are often limited once infrastructure and security costs are considered, the tournament is expected to boost tourism and local spending through the summer.

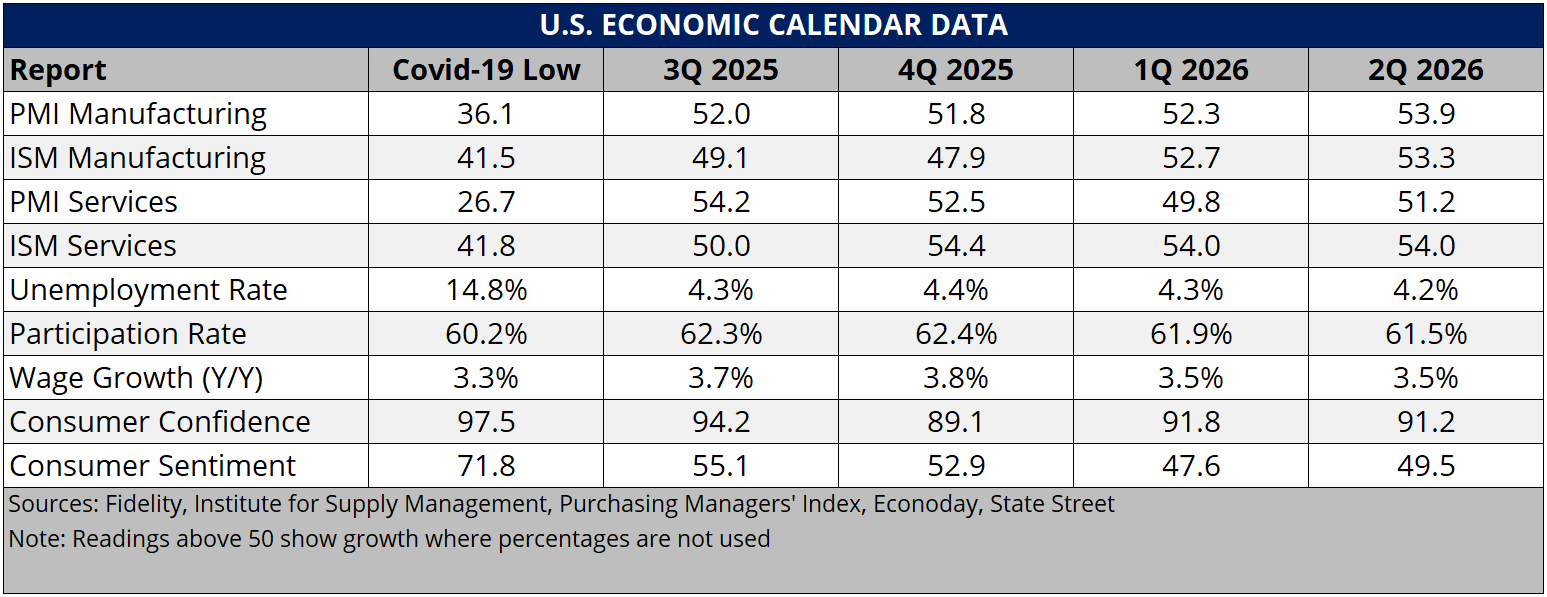

Economic Indicators

The second quarter saw periods of volatility from the ongoing conflict in the Middle East and welcomed a new Federal Reserve Chair in Kevin Warsh but ultimately delivered resilient and stable economic results. Given ongoing concerns and overlooking some partisan impacts, measures of Consumer Confidencei and Consumer Sentimentii remain downcast, as consumers are still worried about the economy, labor market, and inflationary pressures. Despite these concerns, employment dataiii continues to show a market that is light on both hiring and firing, in other words, fairly stable. Similarly, wage pressures are stable, which provides support that a rate hike may not be necessary, and is reassuring, given Kevin Warsh expressed greater inflation concern than what the market was anticipating, and a rate hike could be a risk to growth. Monitoring the Fed is expected to be less certain, given they are expected to provide less forward guidance.

Manufacturing reportsiv,v continue to show growth driven by domestic demand, but are lacking foreign demand due to tariff issues. Service industriesvi,vii showed solid growth and were aided by a boost to demand from the World Cup and related tourism.

Market Impact on Major Asset Classes

Impact on Equities:

The second quarter delivered the best quarterly returns for U.S. large-cap stocks in six years. The S&P 500 rose 15.2% and was propelled by semiconductor stocks as capital expenditures drove company returns higher. AI-driven spending continues to be a key force behind returns: JPMorgan research indicates that companies tied to AI have accounted for roughly 85% of the S&P 500's returns in 2026. While technology performed well in the quarter, industrials remain the top-performing sector in 2026 as investors began to rotate away from growth towards the end of the quarter. While large companies received a lot of attention, small-cap stocks measured by the Russell 2000 performed even better. However, much of the outperformance was generated by low-quality and unprofitable stocks, a sign of speculative behavior.

While the U.S. markets performed well, international stocks continued to outpace them. MSCI Emerging Markets led global markets despite another quarterly decline in China. China has seen substantial AI advances and has an attractively priced market, which warrants monitoring. Taiwan and South Korea continue to be bright spots, while the entire region has both lower valuations and higher earnings expectations compared to much of the rest of the world.

Developed international markets, measured by MSCI EAFE, rose but continue to struggle more than other regions given a lack of productivity growth, geopolitical shocks, and energy disruptions, though increased defense spending remains encouraging.

The MSCI Japan Index slightly lagged the U.S. and rose 14.2%, as its economy continues to improve and corporate reforms benefit the market. Companies saw double-digit earnings growth showing fundamental strength. Further, increased inflation led the Bank of Japan to raise rates to levels not seen in roughly three decades.

With geopolitical volatility unlikely to subside, maintaining a long-term plan and a focus on fundamentals remains essential. Maintaining diversification and exposure to attractive risk-and-return tradeoffs is a better use of energy than reacting to headlines. Looking ahead, there are reasons to remain cautious, such as elevated valuations, strong returns from unprofitable companies, and resilience being increasingly dependent on AI capital expenditures. If AI sentiment falters as companies reassess their return on investment, lower spending could take some air out of the market. At the same time, earnings expectations remain high and have improved from the previous quarter. Diversified investors may be well positioned, as valuations and earnings expectations for U.S. small-caps and international stocks may be even more attractive than those of the largest U.S. stocks. As shared before, the potential for AI developments could be a benefit for these companies, but if developments falter, the less extended valuations may also protect investors on the downside, offering a potentially asymmetric benefit.

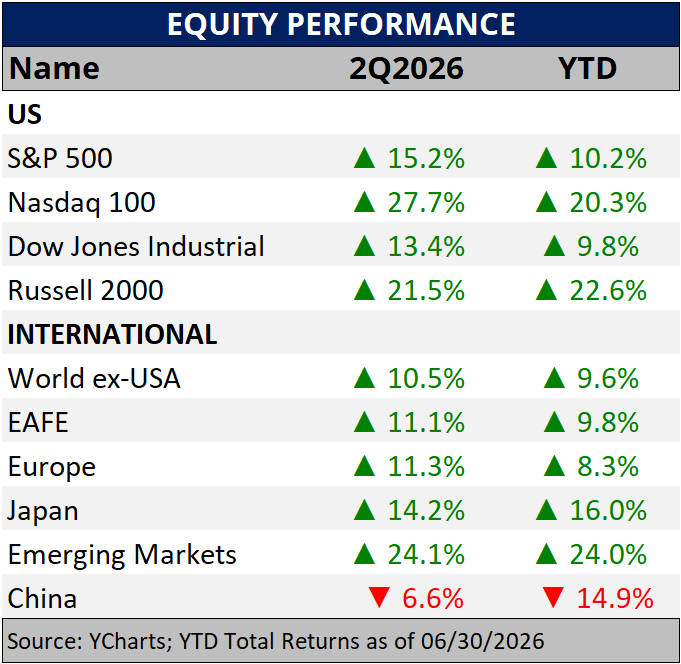

Major World Equity Market Performance

for Q2 2026

Impact on Fixed Income:

Investment grade municipal bonds outperformed corporates and Treasuries in 2Q2026, returning 2.5% vs. 1.4% and 0.3%, respectively. They also lead year to date (YTD), returning 2.3%, driven by continued high demand and a muted reaction in the municipal market to the FOMC meeting. By contrast, short-term Treasury yields rose sharply following Warsh's comments, by as much as 16 basis points (bps; one basis point equals 0.01%), while municipal yields ticked down 1 basis point.

The Treasury curve flattened throughout the quarter as short-end yields rose amid shifting expectations that rates may remain higher for longer. The 2s10s curve, which measures the gap between 2-year and 10-year Treasury yields, tightened from 52bps in April to 30bps by quarter end. In plain terms, investors earned less additional yield for lending over longer periods. Meanwhile, the municipal 2s10s remained at about 50bps through the quarter, providing investors with comparatively more return for extending duration (that is, holding longer-maturity bonds).

Credit spreads remain tight, providing little additional yield for taking on risk. Corporate spreads, which measure the additional yield gained by buying a corporate bond vs. a Treasury bond, dipped from 87bps at the beginning of April to 76bps by the end of June, while the 20-year average was 156bps. For investors, the takeaway is that bonds continue to provide dependable income and portfolio stability, but taking on extra credit risk currently offers little additional reward, reinforcing our preference for high-quality bonds.

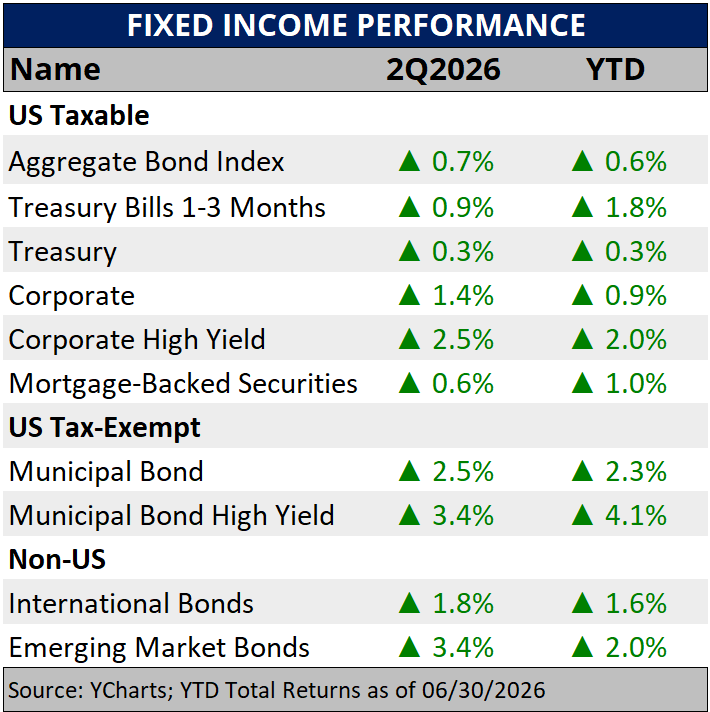

Major Fixed Income Index Returns

for Q2 2026

Impact on Alternatives:

Concentrated stock positions, defined as a single company's stock making up more than 5% of a portfolio, create challenges in portfolio construction and can expose the holder to substantial company-specific risk. These concentrated positions are usually the result of stock awards from a current or former employer, or a good purchase decision of a stock that has done extremely well and now comprises a large portion of the portfolio. High levels of embedded capital gains increase the reluctance to part with a winning position and pay long-term capital gains taxes.

It can be tempting to believe that because these stocks have done well, which is the reason they became large, they will continue a winning trajectory. The evidence contradicts this belief and shows that the risk of significant underperformance, or even a catastrophic loss (defined as a decline greater than 70%), is far higher than most investors assume. Looking at the 10 largest U.S. companies over the past four decades brings back memories of familiar names such as Kodak, IBM, AT&T, General Motors, DuPont, Procter & Gamble, Altria, AIG, and Johnson & Johnson.

Some of these companies no longer exist in their original form, and many others stopped growing and severely underperformed the broader market. A JPMorgan study showed that over 40% of stocks suffer a catastrophic loss, and these losses are almost impossible to predict. Over 70% of stocks that have suffered a catastrophic decline over the past four years were rated either "Buy" or "Strong Buy" by Wall Street analysts.

TMG offers several solutions for managing concentrated stock positions. One of these is called an exchange fund. An exchange fund operates similarly to a diversified mutual fund, but instead of taking cash from investors, it takes stock holdings. As investors contribute different stocks to the fund, the manager aims to track a broad market index, giving investors broad market exposure in exchange for their single stock. After seven years, investors can redeem their interest for a diversified basket of stocks without triggering the capital gains tax that selling the original position would have. The original low-cost basis carries over, meaning taxes are deferred rather than eliminated, but the portfolio gains instant diversification and reduced single-stock risk. Exchange funds involve eligibility requirements and a multi-year commitment, so they are not appropriate for every investor.

Cambridge Associates horizon index Data

as of December 31, 2025

Note: Private market index data is reported on a lag; year-end 2025 figures are the most recent available.

Alternative Investments carry a higher degree of risk related to illiquidity, valuation, and lack of a public market where they can be bought and sold. Investing in Alternative Investments carries the risk of loss to some or all of your principal investment. Alternative Investments that fall under Rule 506 Regulation D of the Investment Company Act of 1940 (“the Act”) are considered unregistered funds, and therefore, are not regulated in the same way as a registered fund under the Act. Depending on the type of investment, a prospective investor must prequalify as an Accredited Investor or Qualified Purchaser under Rule 506 or Qualified Client defined under Rule 205-3 of the Investment Advisers Act of 1940 before investing. Please carefully review the investment’s Private Placement Memorandum (PPM) and/or other Offering Documents and Disclosures before investing in an Alternative Investment.

Looking Ahead

Elevated inflation, higher interest rates, and ongoing geopolitical uncertainty have weighed on consumer confidence for much of the past several years. Despite these concerns, the U.S. economy has remained remarkably resilient. Corporate earnings have generally exceeded expectations, the labor market has remained healthy, and the widely anticipated recession has so far failed to materialize.

Part of this disconnect can be explained by today's "K-shaped" economy. Higher-income households have continued to drive much of the spending and economic growth, while many lower- and middle-income consumers continue to feel pressure from higher prices and borrowing costs. As a result, measures of economic activity have remained relatively strong even as consumer sentiment has stayed historically low.

This difference between perception and reality is an important reminder that investor sentiment and market performance do not always move together. As shown in the chart below, periods of low consumer confidence have historically been followed by some of the strongest market returns. Over the past 55 years, the S&P 500 has averaged a 24.1% return during the 12 months following major sentiment lows, compared with just 4.8% following periods of peak optimism. While history never guarantees future results, it illustrates that markets often begin recovering well before confidence improves.

Today, consumer sentiment remains well below its long-term average despite strong gains in both U.S. and international equity markets. This reinforces the importance of maintaining a long-term perspective rather than allowing headlines or emotions to drive investment decisions.

At The Mather Group, we recognize that uncertainty is an inevitable part of investing. Rather than attempting to predict short-term market movements, we focus on building diversified portfolios grounded in long-term fundamentals, thoughtful risk management, and discipline. History has consistently shown that patient investors who remain focused on their long-term financial goals are better positioned to benefit as markets move through changing economic cycles.

Consumer Confidence and the Stock Market

Peak is defined as the highest index value before a series of higher lows, while a trough is defined as the lowest index value before a series of higher highs. Subsequent 12-month S&P 500 returns are price returns only starting from the end of the month and excluding dividends. Past performance is no guarantee of future results. Data prior to August 2024 adjusted by J.P. Morgan Asset Management to account for methodological changes by the University of Michigan.

Sources

i 2026 U.S. Economic Events & Analysis – Consumer Confidence, Econoday, 6/30/2026

ii 2026 U.S. Economic Events & Analysis – Consumer Sentiment, Econoday, 6/30/2026

iii 2026 U.S. Economic Events & Analysis – Employment Situation, Econoday, 7/2/2026

iv 2026 U.S. Economic Events & Analysis – PMI Manufacturing Final, Econoday, 7/1/2026

v 2026 U.S. Economic Events & Analysis – ISM Manufacturing Index, Econoday, 7/1/2026

vi 2026 U.S. Economic Events & Analysis – PMI Composite Final, Econoday, 7/6/2026

vii 2026 U.S. Economic Events & Analysis – ISM Services Index, Econoday, 7/6/2026

Need more help?

Contact The Mather Group, your advisor, health insurance professional, or your state’s health insurance assistance program (SHIP) for additional information. SHIP is a national program that offers one-on-one Medicare counseling and assistance to individuals and their families.

Key Highlights to Keep You Informed

The second quarter was shaped by geopolitical uncertainty, evolving expectations for interest rates, and continued investment in artificial intelligence (AI). While these developments created periods of market volatility, the underlying economy remained resilient and global markets finished the quarter higher.

Although headlines changed throughout the quarter, our investment approach did not. We remained focused on what we can control: thoughtful portfolio construction, attention to fundamentals, and helping clients stay the course through shifting market conditions.

Geopolitical Uncertainty Increased Market Volatility

Conflict in the Middle East disrupted shipping through the Strait of Hormuz, contributing to higher oil prices and unsettled markets. As diplomatic efforts progressed during June, oil prices moderated and market conditions improved. Although geopolitical risks remain, the quarter served as another reminder that markets often look beyond short-term uncertainty and refocus on long-term economic fundamentals.

U.S. Equities Delivered A Strong Recovery

Following weakness earlier in the year, U.S. stocks rebounded sharply during the second quarter.

- The S&P 500 gained approximately 15%.

- The Nasdaq Composite advanced roughly 21%, its strongest quarterly return since 2020.

Some of the largest cloud and technology companies, the so-called "hyperscalers" that have been heavily investing in data center development, saw their stock prices come under pressure amid concerns that heavy spending may outpace the eventual payoff. Technology companies, particularly semiconductor manufacturers benefiting from continued investment in AI infrastructure, drove much of the market's performance. The rebound underscores the difficulty of timing markets; investors who stayed invested through the spring weakness were rewarded.

The Federal Reserve Entered A New Chapter

Kevin Warsh assumed the role of Federal Reserve Chair during the quarter, replacing Jerome Powell after nearly eight years in the position. Many investors anticipated a more accommodative monetary policy under the new leadership. However, the Federal Open Market Committee elected to leave interest rates unchanged during its June meeting, emphasizing that inflation remains above the Federal Reserve's long-term objective. Future interest rate decisions will continue to be driven by incoming economic data rather than predetermined timelines. For investors, this reinforces the importance of maintaining diversified portfolios that can adapt across a range of economic and interest rate environments.

Artificial Intelligence Remains An Important Investment Theme

Investment in artificial intelligence infrastructure continued at a rapid pace during the quarter. Companies building semiconductors, data storage, networking equipment, and computing capacity benefited from increasing demand, even as investors began questioning whether elevated spending will translate into sustainable long-term earnings growth. That tension was on display in the quarter's most notable market event: SpaceX's long-awaited IPO. The $75 billion offering was the largest ever, surpassing Saudi Aramco's 2019 record of $29.4 billion, and its $1.77 trillion market value against $18.7 billion in 2025 revenue implies roughly 95 times annual revenue, far richer than virtually any other large public company (Nvidia trades near 20 times sales, Palantir at 57). With only about 5% of shares offered to the public, volatility has been elevated. IPOs from other major AI companies, including Anthropic and OpenAI, are anticipated in the coming months. Innovation remains one of the most powerful drivers of long-term economic growth. However, successful investing requires balancing excitement around transformational technologies with careful evaluation of valuations, competitive positioning, and sustainable earnings potential.

Quarterly Market Summary

Returns (USD), as of June 30, 2026

Past performance is not a guarantee of future results. Indices are not available for direct investment. Index performance does not reflect the expenses associated with the management of an actual portfolio.

Market segment (index representation) as follows: US Stock Market (Russell 3000 Index), International Developed Stocks (MSCI World ex USA Index [net dividends]), Emerging Markets (MSCI Emerging Markets Index [net dividends]), Global Real Estate (S&P Global REIT Index [net dividends]), US Bond Market (Bloomberg US Aggregate Bond Index), and Global Bond Market ex US (Bloomberg Global Aggregate ex-USD Bond Index [hedged to USD]). S&P data © 2026 S&P Dow Jones Indices LLC, a division of S&P Global. All rights reserved. Frank Russell Company is the source and owner of the trademarks, service marks, and copyrights related to the Russell Indexes. MSCI data © MSCI 2026, all rights reserved. Bloomberg data provided by Bloomberg.

Notable Events in Q2:

April

Global markets began the quarter facing heightened geopolitical uncertainty as conflict in the Middle East disrupted energy markets and global trade. Oil prices increased while the International Monetary Fund modestly lowered its outlook for global economic growth to 3.1% for 2026. Despite these headwinds, U.S. corporate earnings remained resilient and global stocks rebounded from a weak start to the year.

May

Markets continued to recover from the March downturn related to the conflict in the Middle East as the S&P 500 and Nasdaq both hit new highs, driven by strength in technology stocks. This came despite inflation reaching its highest rate in three years, as the PCE price index, the Fed's preferred inflation measure, rose 3.8% year over year, with oil prices holding near $100 a barrel. May also extended a streak of stronger-than-expected jobs reports as the U.S. economy added 172,000 nonfarm payroll jobs, ahead of the consensus estimate for 85,000, and unemployment held steady at 4.3%.

June

Diplomatic negotiations between the United States and Iran continued throughout June, culminating in a memorandum of understanding on June 17 aimed at ending the conflict. The agreement temporarily eased concerns over global energy supplies, contributing to a decline in Brent crude oil prices from approximately $98 per barrel at the beginning of the month to $71 by month end. While tensions persisted and subsequent events highlighted the fragility of the agreement, lower oil prices helped reduce inflation concerns and improve market sentiment.

Kevin Warsh chaired his first Federal Open Market Committee meeting after succeeding Jerome Powell as Federal Reserve Chair. The Committee left interest rates unchanged at 3.5% to 3.75%, while reaffirming its commitment to returning inflation to its 2% target.

The FIFA World Cup also began during the quarter, with matches hosted across the United States, Canada, and Mexico. While historical evidence suggests the long-term economic benefits for host cities are often limited once infrastructure and security costs are considered, the tournament is expected to boost tourism and local spending through the summer.

Economic Indicators

The second quarter saw periods of volatility from the ongoing conflict in the Middle East and welcomed a new Federal Reserve Chair in Kevin Warsh but ultimately delivered resilient and stable economic results. Given ongoing concerns and overlooking some partisan impacts, measures of Consumer Confidencei and Consumer Sentimentii remain downcast, as consumers are still worried about the economy, labor market, and inflationary pressures. Despite these concerns, employment dataiii continues to show a market that is light on both hiring and firing, in other words, fairly stable. Similarly, wage pressures are stable, which provides support that a rate hike may not be necessary, and is reassuring, given Kevin Warsh expressed greater inflation concern than what the market was anticipating, and a rate hike could be a risk to growth. Monitoring the Fed is expected to be less certain, given they are expected to provide less forward guidance.

Manufacturing reportsiv,v continue to show growth driven by domestic demand, but are lacking foreign demand due to tariff issues. Service industriesvi,vii showed solid growth and were aided by a boost to demand from the World Cup and related tourism.

Market Impact on Major Asset Classes

Impact on Equities:

The second quarter delivered the best quarterly returns for U.S. large-cap stocks in six years. The S&P 500 rose 15.2% and was propelled by semiconductor stocks as capital expenditures drove company returns higher. AI-driven spending continues to be a key force behind returns: JPMorgan research indicates that companies tied to AI have accounted for roughly 85% of the S&P 500's returns in 2026. While technology performed well in the quarter, industrials remain the top-performing sector in 2026 as investors began to rotate away from growth towards the end of the quarter. While large companies received a lot of attention, small-cap stocks measured by the Russell 2000 performed even better. However, much of the outperformance was generated by low-quality and unprofitable stocks, a sign of speculative behavior.

While the U.S. markets performed well, international stocks continued to outpace them. MSCI Emerging Markets led global markets despite another quarterly decline in China. China has seen substantial AI advances and has an attractively priced market, which warrants monitoring. Taiwan and South Korea continue to be bright spots, while the entire region has both lower valuations and higher earnings expectations compared to much of the rest of the world.

Developed international markets, measured by MSCI EAFE, rose but continue to struggle more than other regions given a lack of productivity growth, geopolitical shocks, and energy disruptions, though increased defense spending remains encouraging.

The MSCI Japan Index slightly lagged the U.S. and rose 14.2%, as its economy continues to improve and corporate reforms benefit the market. Companies saw double-digit earnings growth showing fundamental strength. Further, increased inflation led the Bank of Japan to raise rates to levels not seen in roughly three decades.

With geopolitical volatility unlikely to subside, maintaining a long-term plan and a focus on fundamentals remains essential. Maintaining diversification and exposure to attractive risk-and-return tradeoffs is a better use of energy than reacting to headlines. Looking ahead, there are reasons to remain cautious, such as elevated valuations, strong returns from unprofitable companies, and resilience being increasingly dependent on AI capital expenditures. If AI sentiment falters as companies reassess their return on investment, lower spending could take some air out of the market. At the same time, earnings expectations remain high and have improved from the previous quarter. Diversified investors may be well positioned, as valuations and earnings expectations for U.S. small-caps and international stocks may be even more attractive than those of the largest U.S. stocks. As shared before, the potential for AI developments could be a benefit for these companies, but if developments falter, the less extended valuations may also protect investors on the downside, offering a potentially asymmetric benefit.

Major World Equity Market Performance

for Q2 2026

Impact on Fixed Income:

Investment grade municipal bonds outperformed corporates and Treasuries in 2Q2026, returning 2.5% vs. 1.4% and 0.3%, respectively. They also lead year to date (YTD), returning 2.3%, driven by continued high demand and a muted reaction in the municipal market to the FOMC meeting. By contrast, short-term Treasury yields rose sharply following Warsh's comments, by as much as 16 basis points (bps; one basis point equals 0.01%), while municipal yields ticked down 1 basis point.

The Treasury curve flattened throughout the quarter as short-end yields rose amid shifting expectations that rates may remain higher for longer. The 2s10s curve, which measures the gap between 2-year and 10-year Treasury yields, tightened from 52bps in April to 30bps by quarter end. In plain terms, investors earned less additional yield for lending over longer periods. Meanwhile, the municipal 2s10s remained at about 50bps through the quarter, providing investors with comparatively more return for extending duration (that is, holding longer-maturity bonds).

Credit spreads remain tight, providing little additional yield for taking on risk. Corporate spreads, which measure the additional yield gained by buying a corporate bond vs. a Treasury bond, dipped from 87bps at the beginning of April to 76bps by the end of June, while the 20-year average was 156bps. For investors, the takeaway is that bonds continue to provide dependable income and portfolio stability, but taking on extra credit risk currently offers little additional reward, reinforcing our preference for high-quality bonds.

Major Fixed Income Index Returns

for Q2 2026

Impact on Alternatives:

Concentrated stock positions, defined as a single company's stock making up more than 5% of a portfolio, create challenges in portfolio construction and can expose the holder to substantial company-specific risk. These concentrated positions are usually the result of stock awards from a current or former employer, or a good purchase decision of a stock that has done extremely well and now comprises a large portion of the portfolio. High levels of embedded capital gains increase the reluctance to part with a winning position and pay long-term capital gains taxes.

It can be tempting to believe that because these stocks have done well, which is the reason they became large, they will continue a winning trajectory. The evidence contradicts this belief and shows that the risk of significant underperformance, or even a catastrophic loss (defined as a decline greater than 70%), is far higher than most investors assume. Looking at the 10 largest U.S. companies over the past four decades brings back memories of familiar names such as Kodak, IBM, AT&T, General Motors, DuPont, Procter & Gamble, Altria, AIG, and Johnson & Johnson.

Some of these companies no longer exist in their original form, and many others stopped growing and severely underperformed the broader market. A JPMorgan study showed that over 40% of stocks suffer a catastrophic loss, and these losses are almost impossible to predict. Over 70% of stocks that have suffered a catastrophic decline over the past four years were rated either "Buy" or "Strong Buy" by Wall Street analysts.

TMG offers several solutions for managing concentrated stock positions. One of these is called an exchange fund. An exchange fund operates similarly to a diversified mutual fund, but instead of taking cash from investors, it takes stock holdings. As investors contribute different stocks to the fund, the manager aims to track a broad market index, giving investors broad market exposure in exchange for their single stock. After seven years, investors can redeem their interest for a diversified basket of stocks without triggering the capital gains tax that selling the original position would have. The original low-cost basis carries over, meaning taxes are deferred rather than eliminated, but the portfolio gains instant diversification and reduced single-stock risk. Exchange funds involve eligibility requirements and a multi-year commitment, so they are not appropriate for every investor.

Cambridge Associates horizon index Data

as of December 31, 2025

Note: Private market index data is reported on a lag; year-end 2025 figures are the most recent available.

Alternative Investments carry a higher degree of risk related to illiquidity, valuation, and lack of a public market where they can be bought and sold. Investing in Alternative Investments carries the risk of loss to some or all of your principal investment. Alternative Investments that fall under Rule 506 Regulation D of the Investment Company Act of 1940 (“the Act”) are considered unregistered funds, and therefore, are not regulated in the same way as a registered fund under the Act. Depending on the type of investment, a prospective investor must prequalify as an Accredited Investor or Qualified Purchaser under Rule 506 or Qualified Client defined under Rule 205-3 of the Investment Advisers Act of 1940 before investing. Please carefully review the investment’s Private Placement Memorandum (PPM) and/or other Offering Documents and Disclosures before investing in an Alternative Investment.

Looking Ahead

Elevated inflation, higher interest rates, and ongoing geopolitical uncertainty have weighed on consumer confidence for much of the past several years. Despite these concerns, the U.S. economy has remained remarkably resilient. Corporate earnings have generally exceeded expectations, the labor market has remained healthy, and the widely anticipated recession has so far failed to materialize.

Part of this disconnect can be explained by today's "K-shaped" economy. Higher-income households have continued to drive much of the spending and economic growth, while many lower- and middle-income consumers continue to feel pressure from higher prices and borrowing costs. As a result, measures of economic activity have remained relatively strong even as consumer sentiment has stayed historically low.

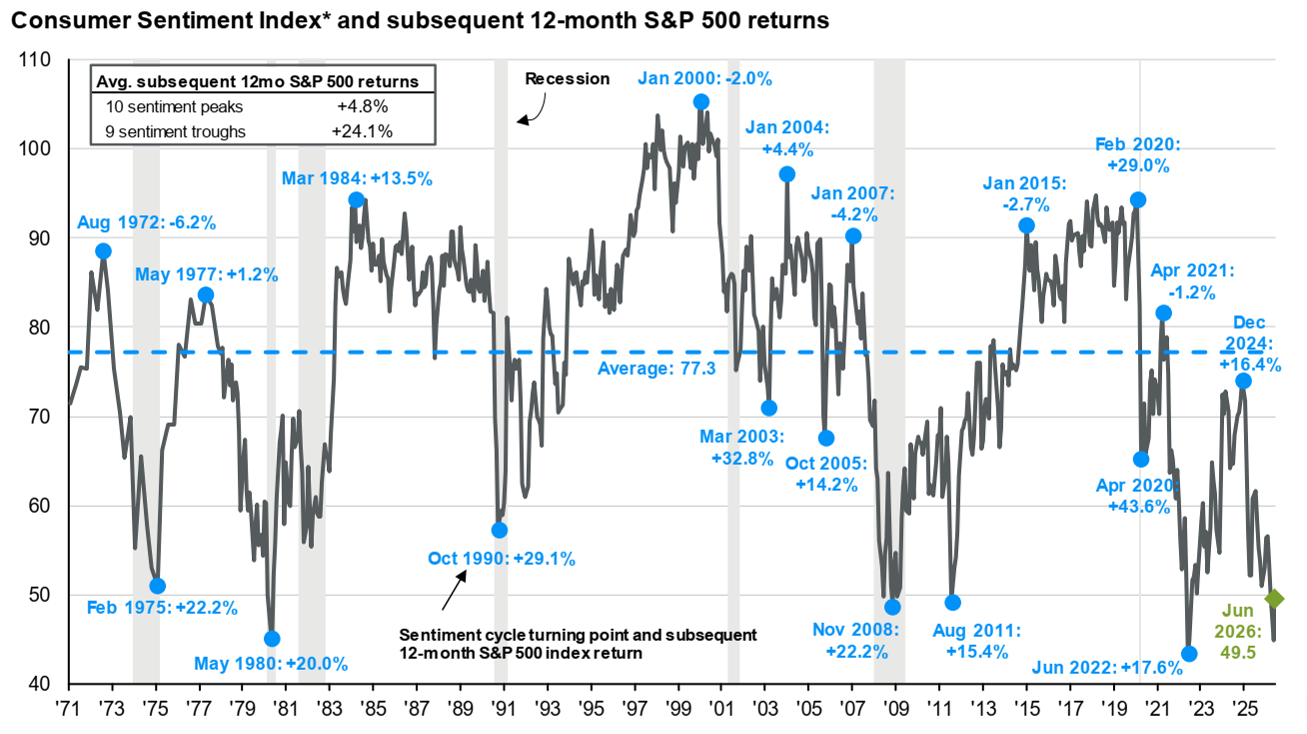

This difference between perception and reality is an important reminder that investor sentiment and market performance do not always move together. As shown in the chart below, periods of low consumer confidence have historically been followed by some of the strongest market returns. Over the past 55 years, the S&P 500 has averaged a 24.1% return during the 12 months following major sentiment lows, compared with just 4.8% following periods of peak optimism. While history never guarantees future results, it illustrates that markets often begin recovering well before confidence improves.

Today, consumer sentiment remains well below its long-term average despite strong gains in both U.S. and international equity markets. This reinforces the importance of maintaining a long-term perspective rather than allowing headlines or emotions to drive investment decisions.

At The Mather Group, we recognize that uncertainty is an inevitable part of investing. Rather than attempting to predict short-term market movements, we focus on building diversified portfolios grounded in long-term fundamentals, thoughtful risk management, and discipline. History has consistently shown that patient investors who remain focused on their long-term financial goals are better positioned to benefit as markets move through changing economic cycles.

Consumer Confidence and the Stock Market

Peak is defined as the highest index value before a series of higher lows, while a trough is defined as the lowest index value before a series of higher highs. Subsequent 12-month S&P 500 returns are price returns only starting from the end of the month and excluding dividends. Past performance is no guarantee of future results. Data prior to August 2024 adjusted by J.P. Morgan Asset Management to account for methodological changes by the University of Michigan.

Sources

i 2026 U.S. Economic Events & Analysis – Consumer Confidence, Econoday, 6/30/2026

ii 2026 U.S. Economic Events & Analysis – Consumer Sentiment, Econoday, 6/30/2026

iii 2026 U.S. Economic Events & Analysis – Employment Situation, Econoday, 7/2/2026

iv 2026 U.S. Economic Events & Analysis – PMI Manufacturing Final, Econoday, 7/1/2026

v 2026 U.S. Economic Events & Analysis – ISM Manufacturing Index, Econoday, 7/1/2026

vi 2026 U.S. Economic Events & Analysis – PMI Composite Final, Econoday, 7/6/2026

vii 2026 U.S. Economic Events & Analysis – ISM Services Index, Econoday, 7/6/2026

Need more help?

Contact The Mather Group, your advisor, health insurance professional, or your state’s health insurance assistance program (SHIP) for additional information. SHIP is a national program that offers one-on-one Medicare counseling and assistance to individuals and their families.

.avif)