What Is a 530A Account? A Guide to Opening and Funding a Child's Account

June 30, 2026

July 4 marks not only the 250th anniversary of the signing of the Declaration of Independence, but also the official launch of 530A accounts, commonly referred to as "Trump Accounts."

Created under the One Big Beautiful Bill (OBBB), these new tax-advantaged accounts are designed to encourage long-term saving and investing for children. Since their introduction, there has been significant interest in how these accounts work, who may benefit, and the role they could play in a long-term financial strategy.

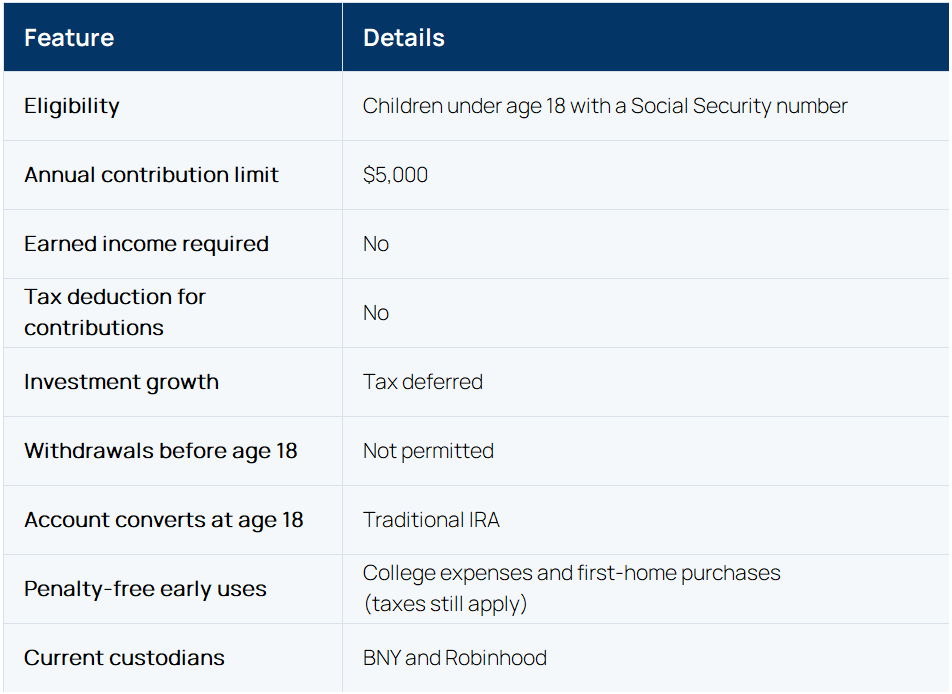

What Is a 530A Account?

A 530A account is a tax-advantaged investment account available to children under age 18 who have a valid Social Security number.

Although these accounts share some similarities with custodial IRAs, they have several unique features.

Key Features of a 530A Account

Additional Features

- Contributions may come from parents, grandparents, family members, friends, employers, or other entities.

- Individual contributions are made with after-tax dollars.

- Unlike a Roth IRA, earned income is not required.

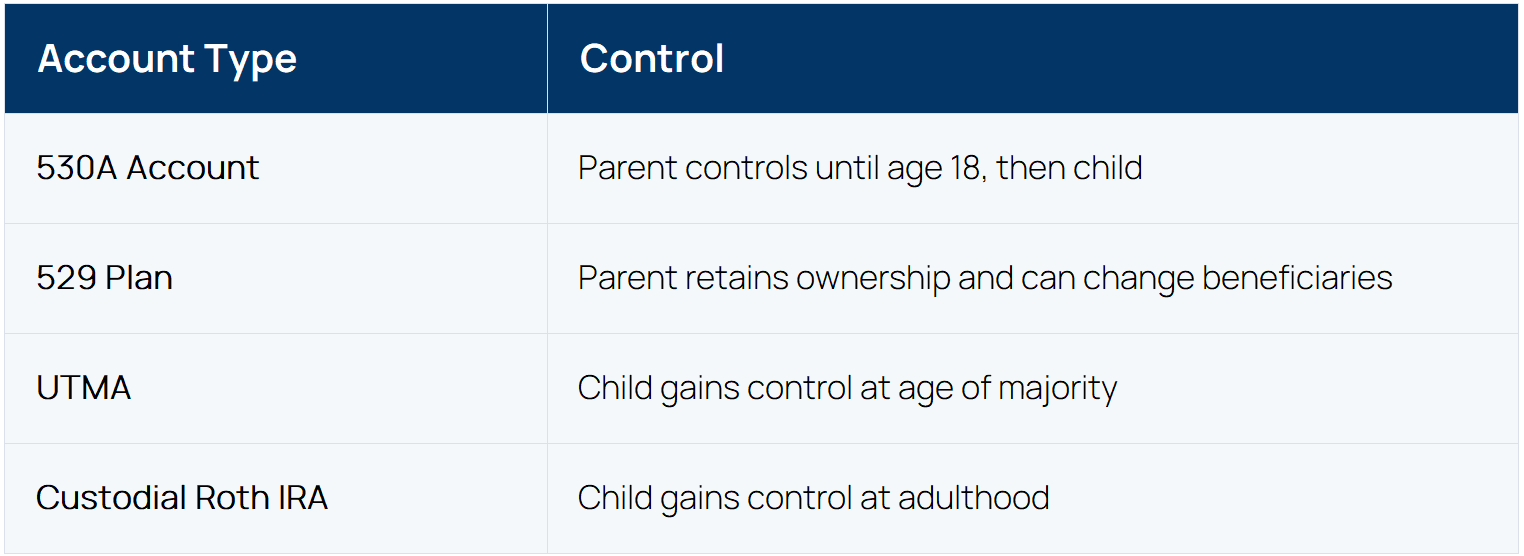

- The child is the legal owner of the account, while a parent or guardian serves as custodian until age 18.

- At age 18, the account converts to a traditional IRA.

Employer Contributions May Provide an Additional Benefit

One unique aspect of 530A accounts is that employers can contribute up to $2,500 annually through a Section 125 cafeteria plan.

These contributions:

- May be made to the employee's account or the accounts of the employee's dependent children.

- Are excluded from the employee's taxable income.

- Can provide another source of savings beyond family contributions.

Should You Open a 530A Account?

For many families, opening an account may make sense simply because of the available contributions.

Federal Seed Contribution

Children born between January 1, 2025, and December 31, 2028, are eligible to receive a $1,000 federal contribution.

Dell Foundation Contribution

Children under age 10 who live in qualifying ZIP codes with median household income below $150,000 may receive a $250 contribution from Michael and Susan Dell.

The Dell contribution is limited to the first 25 million activated accounts.

Currently, approximately six million accounts have already been registered.

The Catch

You only receive these contributions if an account is opened and activated.

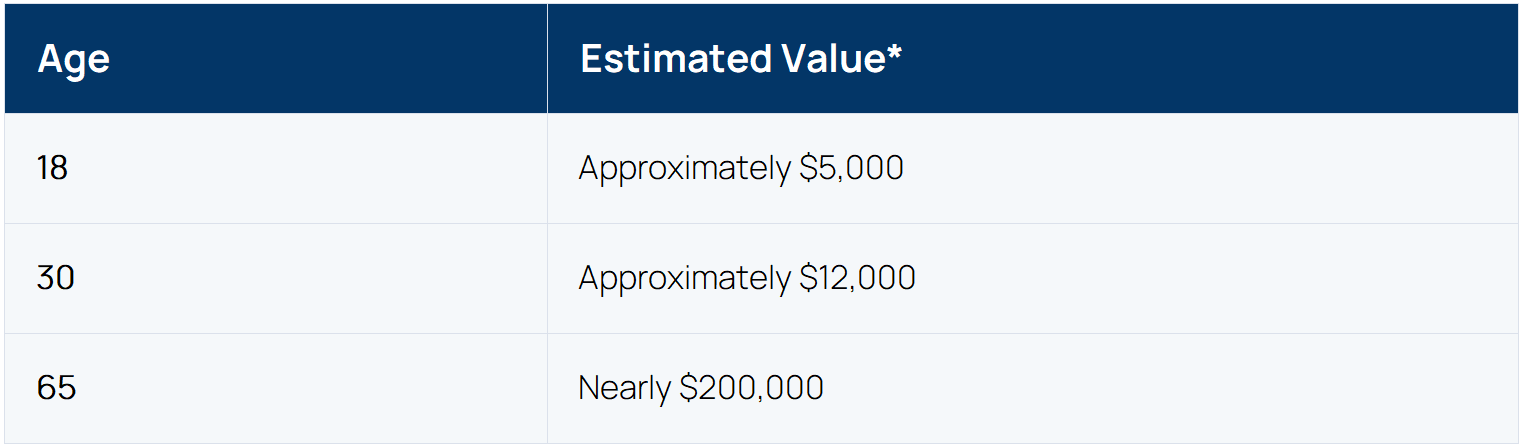

What Could a $1,000 Contribution Potentially Grow To?

While future returns are never guaranteed, long time horizons can have a powerful impact.

Pros and Cons of 530A Accounts

Potential Advantages

- Eligible children may receive a $1,000 federal contribution.

- Additional foundation contributions may be available.

- No earned income requirement.

- Employer contributions may be available.

- Tax-deferred growth.

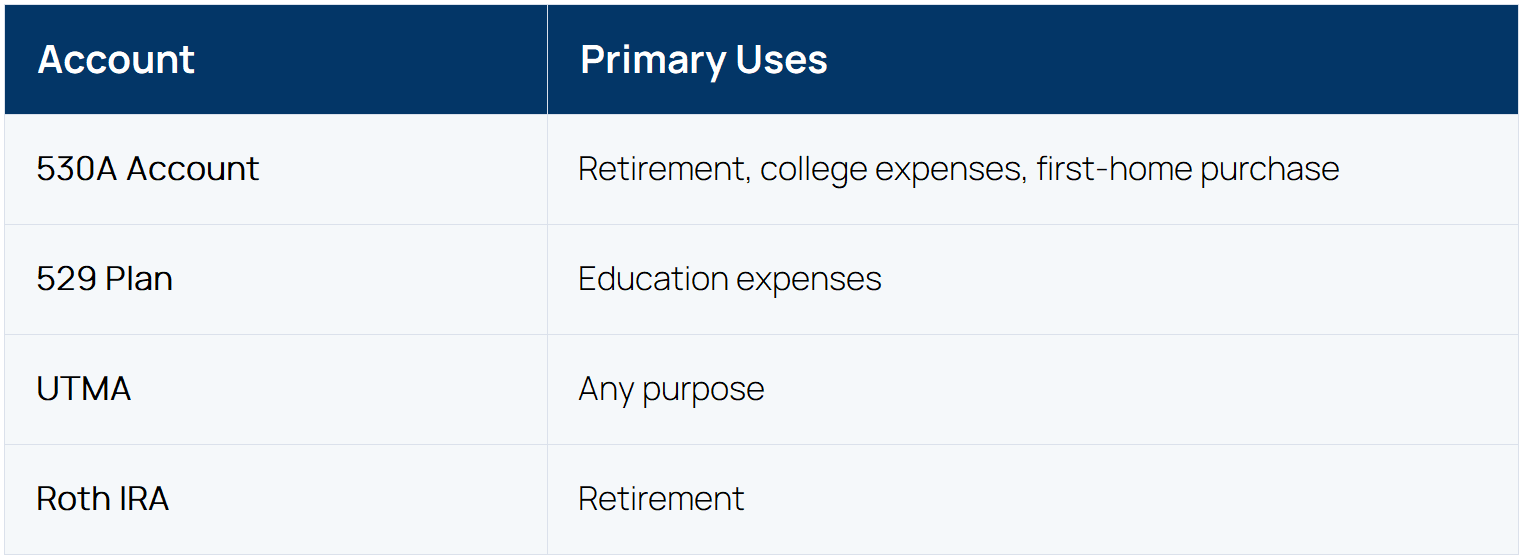

- Funds may be used for retirement, college, or a first home purchase.

- Friends and family members can contribute.

Potential Drawbacks

- Annual contributions are limited to $5,000.

- Individual contributions are not tax deductible.

- Withdrawals are taxable.

- Kiddie tax rules may apply.

- Children gain full control of the account at age 18.

- Funds generally cannot be accessed before age 18.

- Custodian options are currently limited.

- State tax treatment may vary.

Should You Fund a 530A Account With Your Own Money?

Opening an account and funding it are two separate decisions.

Capturing available "free money" may make opening the account worthwhile. Whether your own savings should go into the account depends on your goals and other available options.

Alternatives include:

- 529 plans

- UTMA accounts

- Roth IRAs

When deciding where to save, four factors are particularly important:

- Contribution limits

- Taxes

- Intended use

- Access and control

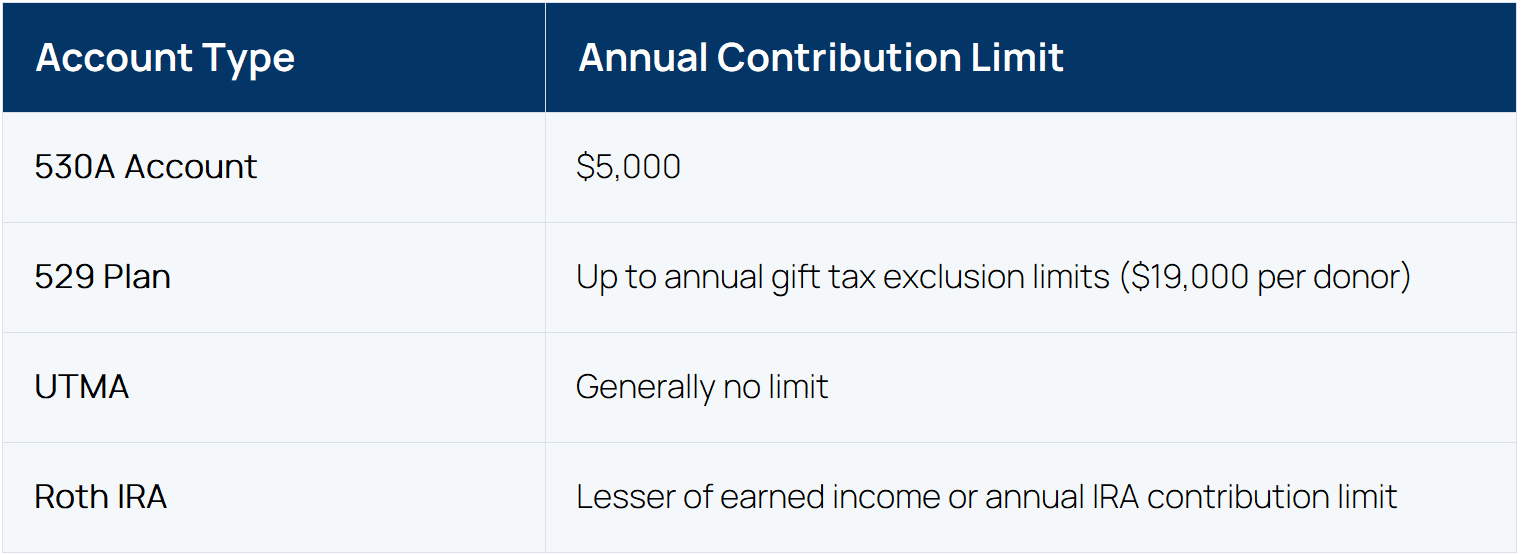

Comparing 530A Accounts With Other Savings Vehicles

Contribution Limits

Because of the relatively low contribution limit, a 530A account may complement rather than replace other savings vehicles.

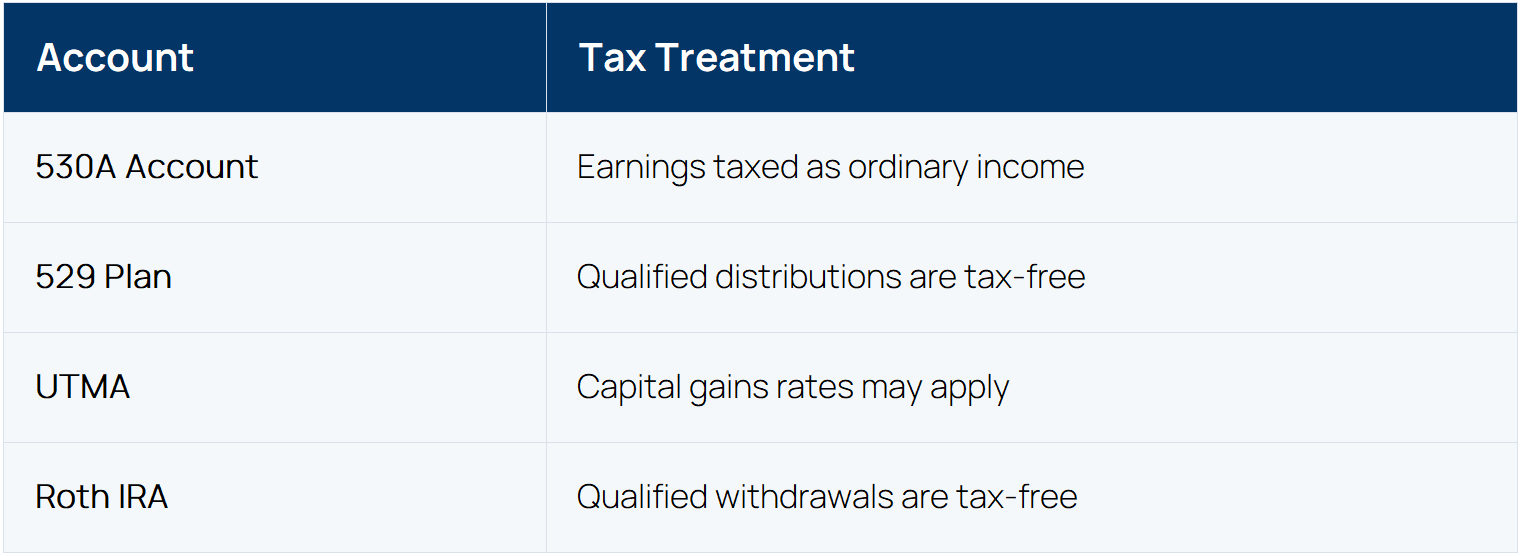

Tax Treatment

All four account types are funded with after-tax dollars. The biggest differences occur when money is withdrawn.

State Tax Benefits

Many states provide tax benefits for 529 contributions.

Individual contributions to 530A accounts do not receive a federal tax deduction, and state treatment may vary.

Some states may not conform to federal rules, meaning:

- Third-party contributions could be taxable.

- Earnings could be taxed annually.

- The account may not receive IRA treatment under state law.

Families should consult their tax advisor regarding their state's rules.

Intended Use

Different accounts are designed for different goals.

Unlike a 529 plan, a 530A account offers greater flexibility beyond education.

However, withdrawals are taxable.

Access and Control

Who controls the money may be just as important as how it is invested.

Parents who value flexibility and ongoing control may prefer 529 plans.

Frequently Asked Questions

Who can open a 530A account?

Parents or legal guardians of dependent children generally may open these accounts.

Grandparents may only open an account if the child is their dependent.

Can grandparents or others contribute?

Yes.

Family members, friends, and other individuals may contribute.

However, gift tax rules should be considered.

How do contributions coordinate with gifting rules?

Current law may require gift tax returns for some contributors.

Unlike 529 plans, contributions to 530A accounts do not qualify for the annual gift tax exclusion because the child cannot access the assets until age 18.

Families should consult their tax advisor before making large gifts.

Are contributions tax deductible?

No.

Individual contributions are made with after-tax dollars.

Employer and foundation contributions are generally pre-tax.

Because both pre-tax and after-tax dollars may exist in the account, basis tracking may become important.

Do children need earned income?

No.

Unlike a Roth IRA, earned income is not required.

Can the money be used for college?

Yes.

College expenses qualify for penalty-free withdrawals.

However, withdrawals are still taxable.

In some cases, the kiddie tax may apply, which could result in a portion of earnings being taxed at the parent's tax rate.

Can the money be used to buy a first home?

Yes.

First-time home purchases qualify for penalty-free withdrawals, although taxes still apply.

When can withdrawals begin?

No withdrawals are allowed until January 1 of the year the child turns 18.

When does the child gain control?

The child assumes full ownership and control at age 18.

Should families wait before making contributions?

Possibly.

Because the annual limit is $5,000 from all sources combined, families may want to understand whether employer contributions or other third-party contributions will be available before fully funding the account.

How Do 530A Accounts Compare With 529 Plans?

One of the most common questions parents are asking is whether a 530A account is better than a 529 plan.

The answer depends on your goals.

A 530A Account May Be Attractive If:

- You want to capture the available federal contribution.

- Employer contributions are available.

- You value flexibility beyond education.

- Retirement savings is a long-term goal.

A 529 Plan May Be More Attractive If:

- Education is the primary goal.

- You want tax-free withdrawals for qualified education expenses.

- You want to maintain control over the assets.

- You expect to contribute more than $5,000 annually.

- Your state offers tax incentives.

For many families, these accounts may complement one another rather than compete.

How Do You Open a 530A Account?

Accounts officially become available beginning July 4.

Eligible families may:

- File IRS Form 4547.

- Open an account through participating custodians.

- Activate the account through the Trump Account app or TrumpAccount.com.

Families who previously registered through TrumpAccounts.gov may need to complete an additional identity verification process.

Because multiple unaffiliated websites exist with similar names, families should verify they are using the appropriate platform.

Bottom Line

For many families, opening a 530A account may make sense simply to capture available contributions.

Whether the account should become the primary savings vehicle for your child is a separate question.

A 530A account can complement other strategies such as 529 plans, Roth IRAs, and custodial accounts. The right approach depends on your family's goals, tax considerations, and the level of flexibility and control they want over the assets.

As with any planning decision, it may be helpful to work with your advisor to determine where each savings dollar can have the greatest long-term impact.

Need more help?

Contact The Mather Group, your advisor, health insurance professional, or your state’s health insurance assistance program (SHIP) for additional information. SHIP is a national program that offers one-on-one Medicare counseling and assistance to individuals and their families.

July 4 marks not only the 250th anniversary of the signing of the Declaration of Independence, but also the official launch of 530A accounts, commonly referred to as "Trump Accounts."

Created under the One Big Beautiful Bill (OBBB), these new tax-advantaged accounts are designed to encourage long-term saving and investing for children. Since their introduction, there has been significant interest in how these accounts work, who may benefit, and the role they could play in a long-term financial strategy.

What Is a 530A Account?

A 530A account is a tax-advantaged investment account available to children under age 18 who have a valid Social Security number.

Although these accounts share some similarities with custodial IRAs, they have several unique features.

Key Features of a 530A Account

Additional Features

- Contributions may come from parents, grandparents, family members, friends, employers, or other entities.

- Individual contributions are made with after-tax dollars.

- Unlike a Roth IRA, earned income is not required.

- The child is the legal owner of the account, while a parent or guardian serves as custodian until age 18.

- At age 18, the account converts to a traditional IRA.

Employer Contributions May Provide an Additional Benefit

One unique aspect of 530A accounts is that employers can contribute up to $2,500 annually through a Section 125 cafeteria plan.

These contributions:

- May be made to the employee's account or the accounts of the employee's dependent children.

- Are excluded from the employee's taxable income.

- Can provide another source of savings beyond family contributions.

Should You Open a 530A Account?

For many families, opening an account may make sense simply because of the available contributions.

Federal Seed Contribution

Children born between January 1, 2025, and December 31, 2028, are eligible to receive a $1,000 federal contribution.

Dell Foundation Contribution

Children under age 10 who live in qualifying ZIP codes with median household income below $150,000 may receive a $250 contribution from Michael and Susan Dell.

The Dell contribution is limited to the first 25 million activated accounts.

Currently, approximately six million accounts have already been registered.

The Catch

You only receive these contributions if an account is opened and activated.

What Could a $1,000 Contribution Potentially Grow To?

While future returns are never guaranteed, long time horizons can have a powerful impact.

Pros and Cons of 530A Accounts

Potential Advantages

- Eligible children may receive a $1,000 federal contribution.

- Additional foundation contributions may be available.

- No earned income requirement.

- Employer contributions may be available.

- Tax-deferred growth.

- Funds may be used for retirement, college, or a first home purchase.

- Friends and family members can contribute.

Potential Drawbacks

- Annual contributions are limited to $5,000.

- Individual contributions are not tax deductible.

- Withdrawals are taxable.

- Kiddie tax rules may apply.

- Children gain full control of the account at age 18.

- Funds generally cannot be accessed before age 18.

- Custodian options are currently limited.

- State tax treatment may vary.

Should You Fund a 530A Account With Your Own Money?

Opening an account and funding it are two separate decisions.

Capturing available "free money" may make opening the account worthwhile. Whether your own savings should go into the account depends on your goals and other available options.

Alternatives include:

- 529 plans

- UTMA accounts

- Roth IRAs

When deciding where to save, four factors are particularly important:

- Contribution limits

- Taxes

- Intended use

- Access and control

Comparing 530A Accounts With Other Savings Vehicles

Contribution Limits

Because of the relatively low contribution limit, a 530A account may complement rather than replace other savings vehicles.

Tax Treatment

All four account types are funded with after-tax dollars. The biggest differences occur when money is withdrawn.

State Tax Benefits

Many states provide tax benefits for 529 contributions.

Individual contributions to 530A accounts do not receive a federal tax deduction, and state treatment may vary.

Some states may not conform to federal rules, meaning:

- Third-party contributions could be taxable.

- Earnings could be taxed annually.

- The account may not receive IRA treatment under state law.

Families should consult their tax advisor regarding their state's rules.

Intended Use

Different accounts are designed for different goals.

Unlike a 529 plan, a 530A account offers greater flexibility beyond education.

However, withdrawals are taxable.

Access and Control

Who controls the money may be just as important as how it is invested.

Parents who value flexibility and ongoing control may prefer 529 plans.

Frequently Asked Questions

Who can open a 530A account?

Parents or legal guardians of dependent children generally may open these accounts.

Grandparents may only open an account if the child is their dependent.

Can grandparents or others contribute?

Yes.

Family members, friends, and other individuals may contribute.

However, gift tax rules should be considered.

How do contributions coordinate with gifting rules?

Current law may require gift tax returns for some contributors.

Unlike 529 plans, contributions to 530A accounts do not qualify for the annual gift tax exclusion because the child cannot access the assets until age 18.

Families should consult their tax advisor before making large gifts.

Are contributions tax deductible?

No.

Individual contributions are made with after-tax dollars.

Employer and foundation contributions are generally pre-tax.

Because both pre-tax and after-tax dollars may exist in the account, basis tracking may become important.

Do children need earned income?

No.

Unlike a Roth IRA, earned income is not required.

Can the money be used for college?

Yes.

College expenses qualify for penalty-free withdrawals.

However, withdrawals are still taxable.

In some cases, the kiddie tax may apply, which could result in a portion of earnings being taxed at the parent's tax rate.

Can the money be used to buy a first home?

Yes.

First-time home purchases qualify for penalty-free withdrawals, although taxes still apply.

When can withdrawals begin?

No withdrawals are allowed until January 1 of the year the child turns 18.

When does the child gain control?

The child assumes full ownership and control at age 18.

Should families wait before making contributions?

Possibly.

Because the annual limit is $5,000 from all sources combined, families may want to understand whether employer contributions or other third-party contributions will be available before fully funding the account.

How Do 530A Accounts Compare With 529 Plans?

One of the most common questions parents are asking is whether a 530A account is better than a 529 plan.

The answer depends on your goals.

A 530A Account May Be Attractive If:

- You want to capture the available federal contribution.

- Employer contributions are available.

- You value flexibility beyond education.

- Retirement savings is a long-term goal.

A 529 Plan May Be More Attractive If:

- Education is the primary goal.

- You want tax-free withdrawals for qualified education expenses.

- You want to maintain control over the assets.

- You expect to contribute more than $5,000 annually.

- Your state offers tax incentives.

For many families, these accounts may complement one another rather than compete.

How Do You Open a 530A Account?

Accounts officially become available beginning July 4.

Eligible families may:

- File IRS Form 4547.

- Open an account through participating custodians.

- Activate the account through the Trump Account app or TrumpAccount.com.

Families who previously registered through TrumpAccounts.gov may need to complete an additional identity verification process.

Because multiple unaffiliated websites exist with similar names, families should verify they are using the appropriate platform.

Bottom Line

For many families, opening a 530A account may make sense simply to capture available contributions.

Whether the account should become the primary savings vehicle for your child is a separate question.

A 530A account can complement other strategies such as 529 plans, Roth IRAs, and custodial accounts. The right approach depends on your family's goals, tax considerations, and the level of flexibility and control they want over the assets.

As with any planning decision, it may be helpful to work with your advisor to determine where each savings dollar can have the greatest long-term impact.

Need more help?

Contact The Mather Group, your advisor, health insurance professional, or your state’s health insurance assistance program (SHIP) for additional information. SHIP is a national program that offers one-on-one Medicare counseling and assistance to individuals and their families.

.avif)