A High-Net-Worth Investor's Guide to Choosing a Financial Advisor

June 12, 2026

As wealth grows, financial decisions often become more interconnected. Investment strategy, taxes, retirement income, estate planning, and family goals rarely exist in isolation.

As a result, the challenge often shifts from accumulating assets to coordinating the decisions surrounding them.

The following questions and considerations can help high-net-worth individuals and families evaluate whether professional guidance may provide value and how to assess potential advisory relationships.

What Does a Financial Advisor Do for High-Net-Worth Investors?

For high-net-worth individuals and families, the role of a financial advisor often extends far beyond investment selection.

A comprehensive advisory relationship may help coordinate:

- Investment strategy and portfolio allocation

- Retirement income planning

- Tax-efficient withdrawal strategies

- Social Security and required distribution planning

- Estate and legacy planning

- Charitable giving strategies

- Equity compensation and concentrated stock positions

- Business ownership and liquidity events

- Multigenerational wealth planning

The objective is not simply managing investments. It is helping ensure that investment decisions, taxes, retirement income, estate planning, and family goals work together within a coordinated framework designed to support long-term objectives.

Do I Need a Financial Advisor if I Already Manage My Own Investments?

Many investors are comfortable managing their own portfolios.

However, as financial complexity increases, the value of professional guidance often lies less in selecting investments and more in coordinating decisions across multiple areas of wealth.

For example, retirement withdrawal strategies, tax considerations, and estate planning decisions may influence how investments should be positioned and managed over time.

Many high-net-worth investors seek professional guidance not because they cannot manage investments themselves, but because they recognize that complexity often creates opportunities and risks that extend beyond portfolio management.

Many investors work with an advisor not because they cannot manage investments, but because they want a structured framework that connects financial decisions to broader life goals.

What Financial Complexities Often Arise for High-Net-Worth Families?

As wealth grows, investors may encounter planning considerations such as:

- Managing tax exposure across taxable, retirement, and trust accounts

- Diversifying concentrated stock positions

- Coordinating retirement income strategies

- Navigating required minimum distributions

- Planning for a business transition or liquidity event

- Evaluating estate planning structures

- Integrating charitable giving into the financial plan

- Preparing for the transfer of wealth to future generations

- Coordinating investments with trust and legacy strategies

These issues often interact with one another, making coordinated financial planning increasingly valuable.

What Is a Fiduciary?

Many investors assume all financial advisors are held to the same standard and compensated in the same way. How advice is delivered and how advisors are paid can vary significantly.

Understanding these differences is important because they can influence how recommendations are made and how potential conflicts are managed.

A fiduciary is a financial advisor who is legally and ethically obligated to place the client's interests ahead of their own.

In practical terms, a fiduciary's responsibility is to provide advice based on what they believe is best for the client, not what may generate the highest compensation or benefit the advisor or firm.

Many investors are surprised to learn that not all financial professionals are held to the same fiduciary standard.

Understanding whether an advisor acts as a fiduciary is one of the most important questions an investor can ask.

What Is the Difference Between an RIA and a Broker-Dealer?

While both Registered Investment Advisors (RIAs) and broker-dealers may provide valuable financial guidance, there are important differences in how advice is delivered and how advisors are compensated.

Understanding these distinctions can help investors evaluate how advice is delivered and whether the structure of the relationship aligns with their preferences and long-term goals.

The Mather Group is an independent, fee-only Registered Investment Advisor providing comprehensive wealth management and coordinated financial planning. Rather than focusing solely on investments, we help clients integrate investment strategy, retirement planning, tax considerations, and estate planning into one cohesive framework.

What Is the Difference Between Fee-Only and Commission-Based Advisors?

Another important distinction investors should understand is how financial advisors are compensated.

Fee-Only Advisors

The Mather Group is a Fee-Only Registered Investment Advisor. Fee-only advisors are compensated directly by their clients through advisory fees or financial planning fees and do not receive commissions from financial products.

Because compensation comes directly from the client relationship, fee-only advisors do not have financial incentives tied to selling insurance products, annuities, or proprietary investments.

For many investors, this structure provides greater transparency around how advice is delivered.

Commission-Based Advisors

Commission-based advisors may receive compensation when clients purchase certain financial products, including annuities, insurance policies, mutual funds, or other investments.

Hybrid advisors combine advisory fees with commissions from certain products.

Compensation structure alone does not determine the quality of advice. However, understanding how an advisor is paid can provide valuable insight into how recommendations are made and whether potential conflicts may exist.

As a fee-only Registered Investment Advisor, The Mather Group does not sell financial products and does not accept commissions.

Our focus is delivering comprehensive wealth management and coordinated financial planning, helping clients align investment strategy, retirement planning, tax considerations, and estate planning so the pieces of their financial lives work together, not in isolation.

How Should I Evaluate a Financial Advisor?

When evaluating potential advisors, investors should consider several important factors.

Fiduciary Standard

Does the advisor act as a fiduciary?

Compensation Structure

Is the advisor fee-only, commission-based, or operating under a hybrid model?

Services Provided

Does the relationship include comprehensive financial planning or primarily investment management?

Professional Credentials

Does the advisor hold professional designations such as the Certified Financial Planner™ (CFP®) credential?

Planning Philosophy

Does the advisor emphasize coordinated planning across investments, taxes, retirement income, and estate considerations?

Team Structure

Will you work with a single advisor, or do you benefit from a team of specialists supporting your financial plan?

High-Net-Worth Investor Checklist

You may benefit from coordinated financial planning if you find yourself asking questions such as:

- How should I structure retirement income over the next 20 to 30 years?

- How can I manage taxes across taxable, retirement, and trust accounts?

- Should I diversify a concentrated stock position or employer equity?

- How should my portfolio evolve as retirement approaches?

- How should wealth be transferred to children, grandchildren, or charitable organizations?

- How do investment decisions affect tax exposure and estate planning?

- What happens to my spouse or family if something happens to me?

- Are my beneficiaries, trusts, and estate documents aligned with my current wishes?

- Am I making the most of charitable giving opportunities?

- How should I think about healthcare costs and long-term care planning?

- How do I prepare financially for aging parents or family caregiving responsibilities?

- Have I experienced a major life event such as retirement, widowhood, divorce, the sale of a business, or receiving an inheritance?

- Do I have stock options, RSUs, deferred compensation, or other executive benefits that require coordination?

- Is my portfolio aligned with the goals I have for my family and the legacy I want to leave?

- Have I outgrown a purely investment-focused relationship?

- Am I making important financial decisions in isolation rather than understanding how they affect one another?

If several of these questions resonate with you, it may indicate that financial decisions are becoming increasingly interconnected and that a coordinated planning approach could provide additional clarity and confidence.

Bringing Financial Planning Together

For many high-net-worth individuals and families, the value of a financial advisor extends far beyond investment performance.

It lies in bringing clarity to complexity and ensuring that the many decisions surrounding wealth work together in support of long-term goals.

A thoughtful and coordinated approach can help individuals evaluate tradeoffs, identify opportunities, and make important financial decisions with greater confidence.

Get Clarity on Your Money and Your Plan

At The Mather Group, we believe wealth management involves more than managing investments. Through coordinated planning, we help clients align investment strategy, retirement planning, tax considerations, and estate planning to support the life they want to live.

Schedule a Complimentary Consultation and Personalized Financial Analysis

Before making any commitments, we'll provide a complimentary analysis of your investments, retirement strategy, tax considerations, and estate planning opportunities, helping you understand how the pieces of your financial life fit together and identify opportunities you may not have considered.

Need more help?

Contact The Mather Group, your advisor, health insurance professional, or your state’s health insurance assistance program (SHIP) for additional information. SHIP is a national program that offers one-on-one Medicare counseling and assistance to individuals and their families.

As wealth grows, financial decisions often become more interconnected. Investment strategy, taxes, retirement income, estate planning, and family goals rarely exist in isolation.

As a result, the challenge often shifts from accumulating assets to coordinating the decisions surrounding them.

The following questions and considerations can help high-net-worth individuals and families evaluate whether professional guidance may provide value and how to assess potential advisory relationships.

What Does a Financial Advisor Do for High-Net-Worth Investors?

For high-net-worth individuals and families, the role of a financial advisor often extends far beyond investment selection.

A comprehensive advisory relationship may help coordinate:

- Investment strategy and portfolio allocation

- Retirement income planning

- Tax-efficient withdrawal strategies

- Social Security and required distribution planning

- Estate and legacy planning

- Charitable giving strategies

- Equity compensation and concentrated stock positions

- Business ownership and liquidity events

- Multigenerational wealth planning

The objective is not simply managing investments. It is helping ensure that investment decisions, taxes, retirement income, estate planning, and family goals work together within a coordinated framework designed to support long-term objectives.

Do I Need a Financial Advisor if I Already Manage My Own Investments?

Many investors are comfortable managing their own portfolios.

However, as financial complexity increases, the value of professional guidance often lies less in selecting investments and more in coordinating decisions across multiple areas of wealth.

For example, retirement withdrawal strategies, tax considerations, and estate planning decisions may influence how investments should be positioned and managed over time.

Many high-net-worth investors seek professional guidance not because they cannot manage investments themselves, but because they recognize that complexity often creates opportunities and risks that extend beyond portfolio management.

Many investors work with an advisor not because they cannot manage investments, but because they want a structured framework that connects financial decisions to broader life goals.

What Financial Complexities Often Arise for High-Net-Worth Families?

As wealth grows, investors may encounter planning considerations such as:

- Managing tax exposure across taxable, retirement, and trust accounts

- Diversifying concentrated stock positions

- Coordinating retirement income strategies

- Navigating required minimum distributions

- Planning for a business transition or liquidity event

- Evaluating estate planning structures

- Integrating charitable giving into the financial plan

- Preparing for the transfer of wealth to future generations

- Coordinating investments with trust and legacy strategies

These issues often interact with one another, making coordinated financial planning increasingly valuable.

What Is a Fiduciary?

Many investors assume all financial advisors are held to the same standard and compensated in the same way. How advice is delivered and how advisors are paid can vary significantly.

Understanding these differences is important because they can influence how recommendations are made and how potential conflicts are managed.

A fiduciary is a financial advisor who is legally and ethically obligated to place the client's interests ahead of their own.

In practical terms, a fiduciary's responsibility is to provide advice based on what they believe is best for the client, not what may generate the highest compensation or benefit the advisor or firm.

Many investors are surprised to learn that not all financial professionals are held to the same fiduciary standard.

Understanding whether an advisor acts as a fiduciary is one of the most important questions an investor can ask.

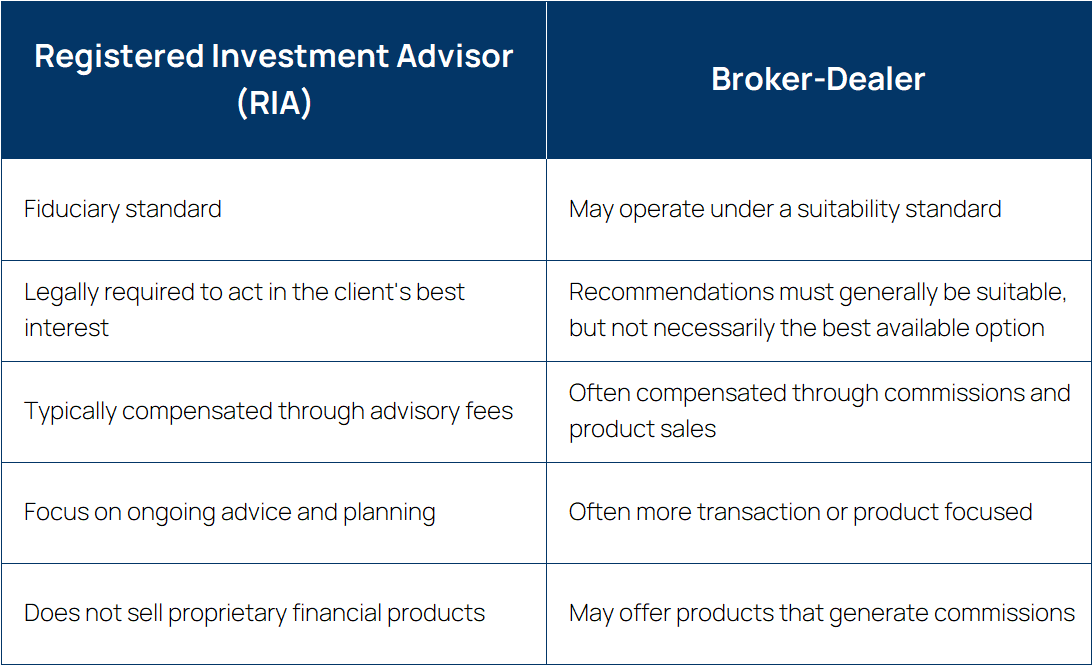

What Is the Difference Between an RIA and a Broker-Dealer?

While both Registered Investment Advisors (RIAs) and broker-dealers may provide valuable financial guidance, there are important differences in how advice is delivered and how advisors are compensated.

Understanding these distinctions can help investors evaluate how advice is delivered and whether the structure of the relationship aligns with their preferences and long-term goals.

The Mather Group is an independent, fee-only Registered Investment Advisor providing comprehensive wealth management and coordinated financial planning. Rather than focusing solely on investments, we help clients integrate investment strategy, retirement planning, tax considerations, and estate planning into one cohesive framework.

What Is the Difference Between Fee-Only and Commission-Based Advisors?

Another important distinction investors should understand is how financial advisors are compensated.

Fee-Only Advisors

The Mather Group is a Fee-Only Registered Investment Advisor. Fee-only advisors are compensated directly by their clients through advisory fees or financial planning fees and do not receive commissions from financial products.

Because compensation comes directly from the client relationship, fee-only advisors do not have financial incentives tied to selling insurance products, annuities, or proprietary investments.

For many investors, this structure provides greater transparency around how advice is delivered.

Commission-Based Advisors

Commission-based advisors may receive compensation when clients purchase certain financial products, including annuities, insurance policies, mutual funds, or other investments.

Hybrid advisors combine advisory fees with commissions from certain products.

Compensation structure alone does not determine the quality of advice. However, understanding how an advisor is paid can provide valuable insight into how recommendations are made and whether potential conflicts may exist.

As a fee-only Registered Investment Advisor, The Mather Group does not sell financial products and does not accept commissions.

Our focus is delivering comprehensive wealth management and coordinated financial planning, helping clients align investment strategy, retirement planning, tax considerations, and estate planning so the pieces of their financial lives work together, not in isolation.

How Should I Evaluate a Financial Advisor?

When evaluating potential advisors, investors should consider several important factors.

Fiduciary Standard

Does the advisor act as a fiduciary?

Compensation Structure

Is the advisor fee-only, commission-based, or operating under a hybrid model?

Services Provided

Does the relationship include comprehensive financial planning or primarily investment management?

Professional Credentials

Does the advisor hold professional designations such as the Certified Financial Planner™ (CFP®) credential?

Planning Philosophy

Does the advisor emphasize coordinated planning across investments, taxes, retirement income, and estate considerations?

Team Structure

Will you work with a single advisor, or do you benefit from a team of specialists supporting your financial plan?

High-Net-Worth Investor Checklist

You may benefit from coordinated financial planning if you find yourself asking questions such as:

- How should I structure retirement income over the next 20 to 30 years?

- How can I manage taxes across taxable, retirement, and trust accounts?

- Should I diversify a concentrated stock position or employer equity?

- How should my portfolio evolve as retirement approaches?

- How should wealth be transferred to children, grandchildren, or charitable organizations?

- How do investment decisions affect tax exposure and estate planning?

- What happens to my spouse or family if something happens to me?

- Are my beneficiaries, trusts, and estate documents aligned with my current wishes?

- Am I making the most of charitable giving opportunities?

- How should I think about healthcare costs and long-term care planning?

- How do I prepare financially for aging parents or family caregiving responsibilities?

- Have I experienced a major life event such as retirement, widowhood, divorce, the sale of a business, or receiving an inheritance?

- Do I have stock options, RSUs, deferred compensation, or other executive benefits that require coordination?

- Is my portfolio aligned with the goals I have for my family and the legacy I want to leave?

- Have I outgrown a purely investment-focused relationship?

- Am I making important financial decisions in isolation rather than understanding how they affect one another?

If several of these questions resonate with you, it may indicate that financial decisions are becoming increasingly interconnected and that a coordinated planning approach could provide additional clarity and confidence.

Bringing Financial Planning Together

For many high-net-worth individuals and families, the value of a financial advisor extends far beyond investment performance.

It lies in bringing clarity to complexity and ensuring that the many decisions surrounding wealth work together in support of long-term goals.

A thoughtful and coordinated approach can help individuals evaluate tradeoffs, identify opportunities, and make important financial decisions with greater confidence.

Get Clarity on Your Money and Your Plan

At The Mather Group, we believe wealth management involves more than managing investments. Through coordinated planning, we help clients align investment strategy, retirement planning, tax considerations, and estate planning to support the life they want to live.

Schedule a Complimentary Consultation and Personalized Financial Analysis

Before making any commitments, we'll provide a complimentary analysis of your investments, retirement strategy, tax considerations, and estate planning opportunities, helping you understand how the pieces of your financial life fit together and identify opportunities you may not have considered.

Need more help?

Contact The Mather Group, your advisor, health insurance professional, or your state’s health insurance assistance program (SHIP) for additional information. SHIP is a national program that offers one-on-one Medicare counseling and assistance to individuals and their families.

.avif)